![]() Download here the complete index of the Leanus manual

Download here the complete index of the Leanus manual

Rating systems, algorithms for calculating PD, artificial intelligence and in general automatic creditworthiness assessment tools are now part of all corporate risk assessment models and compete with the human being's ability to decide and interpret .

Intelligent systems, which for some would do even better than human beings, can no longer do without them, given the need for operators to manage large volumes in a short time and to standardize evaluation criteria.

Everyone agrees on the need to have tools to support decision-making processes and information "collectors" capable of organizing and synthesizing large amounts of data; on the other hand, not everyone agrees on how to use the information and on the logical-organizational process that must lead to risk assessment.

On the one hand, the so-called Algorithm-centric models, on the other hand, the models that see the strong point of the valuation model in the role of the Credit Manager

Whatever the point of view, everyone agrees that the models adopted so far have not proved to be infallible; if the rating systems adopted up to now had been, there would have been no growth in NPL registered in recent years.

Common sense should lead to mediation, that is, to an approach based both on the use of automatic evaluation systems and on the ability and above all on people's skills.

But what is the orientation of the banking system?

A good benchmark is offered by Bank of Italy than with his system ICAS (In-house Credit Assessment System, used by seven other European countries) states the principle according to which "in accordance with the Eurosystem's provisions on credit assessment systems, the assessment must be based on a statistical component (ICAS Stat) and on a subsequent stage of qualitative and quantitative assessment by financial analysts (Expert System).

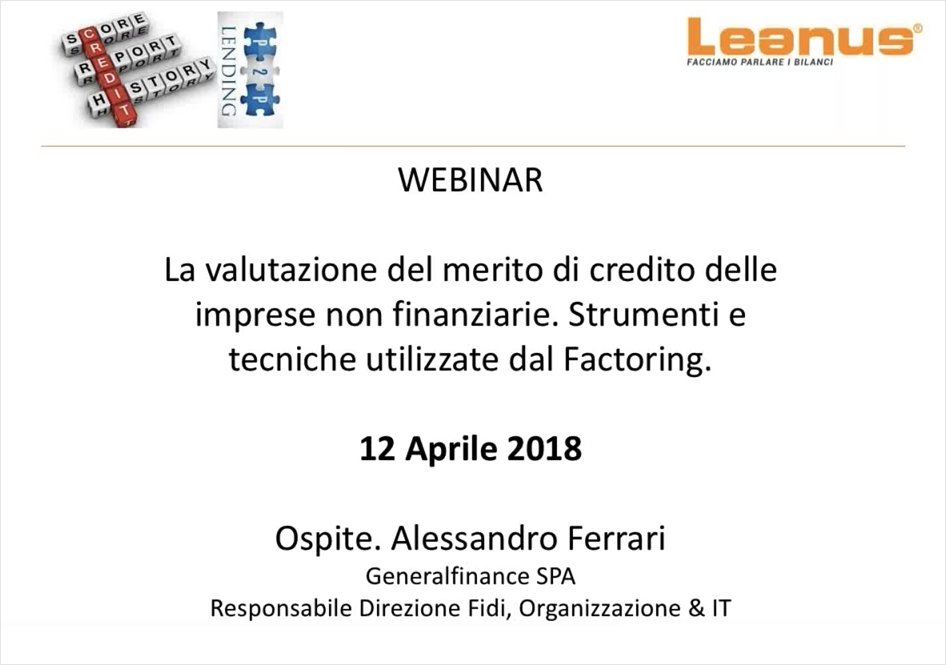

In addition to that of the Bank of Italy, another example comes from the financial world and in particular from general finance, one of the main factoring companies whose valuation model is well described in the webinar by the Head of Loans and Organization Alessandro Ferrari

Some interesting aspects emerge from the interview

- Rating systems lead to different, sometimes discordant, results for the same individuals or groups of companies. (see comparison between Leanus, Cerved, Euler financial statements)

- The risk is not an absolute principle but a relative one, that is, it depends on the person who evaluates the counterparty; from this it follows that each subject needs to refine his own evaluation model.

- Although some elements cannot be neglected for the purpose of identifying the signs of crisis, it is extremely complex to identify a set of parameters capable of anticipating the business situation well in advance. Just to give an example, as published in Milano Finanza on 24 February in the article entitled "On the trail of stress", only 42 of the 15.000 (Revenues greater than one million Euros) that had negative Net Equity in 2015, are currently go to default; less than 3 per thousand. It follows that even the simple use of parameters that indisputably indicate a potential state of crisis can lead to the exclusion of subjects who, despite having a highly compromised accounting profile, have put in place plans, resources and strategies capable of returning to equilibrium. Conversely, the use of other indicators, even if sophisticated, does not necessarily make it possible to anticipate a default.

In a nutshell, it could be concluded that the reliability assessment activity cannot ignore the acceptance of a certain level of error and therefore of losses associated with it; Excessive use of technology to date has proved not to be sufficient (see trend NPL and in general the actual ability of the system to adjust the disbursement of credit and the relative prices to the actual corporate risk profile); in the meantime, perhaps due to excessive expectations towards automatic systems, the opportunity was lost to invest as much as necessary in skills, continuing to adequately train the credit managers of the future.

One last note. Like it or not, for large banking groups with an internal rating system, the ECB uses the rating and relative PD as the only measure of collateral in monetary policy operations. What does it mean? It means that a bank that needs liquidity can pledge its portfolio of loans, as long as the ratings of the borrowers are not below a certain threshold. On this basis the ECB provides the necessary liquidity. Banks that do not have an internal rating system, on the other hand, interact with the Bank of Italy and in particular with the group ICAS which, contrary to ECB, alongside the rating system the expert system, or the judgment of a team of experts who can modify the automatic judgment. Two alternative models that coexist within the same system.

Post your feedback on this topic.