Guide to evaluate the quality of the financial statements received from your infoprovider

It may seem strange but despite the term "Statutory financial statements" makes us think of a standard format that is the same for everyone and such as to leave little room for differences in quality, behind the provision of official statutory financial statements, such macroscopic differences can be hidden as to influence, sometimes significantly, the quality of the service based on the use of information in it contained. Below are some elements that should be considered to evaluate the quality of the supply - price excluded. Below are some examples of extractions carried out with Leanus that provide an indication of the number of financial statements that could present problems.

- Completeness and correctness of the data, or correspondence between Assets and Liabilities (The balance does not square !!!!, about a hundred cases in total) and between Account Items and the sum of the corresponding Sub-Account items (the sum does not make up the total !!!!, about 5-10%)

- Degree of updating that is, days elapsed between receipt from the supplier (via batch or other systems) and the availability of the same balance sheet at the Business Register.

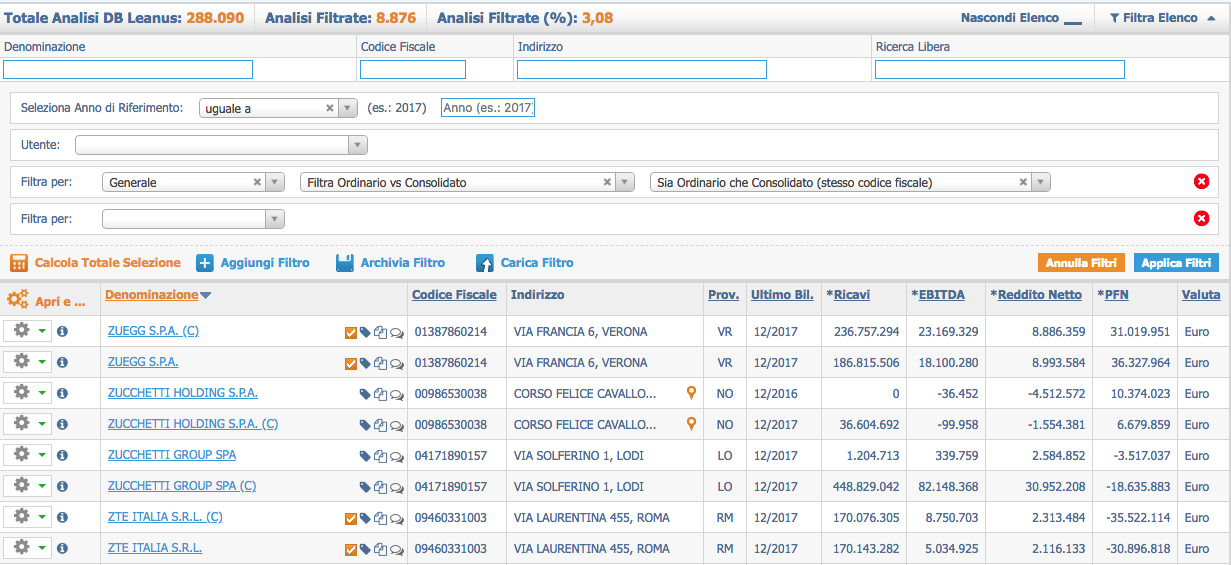

- Availability, if existing for the same subject with the same CF / VAT number, both of Ordinary and Consolidated financial statements

- Processing and integration in the accounting prospectus (generally abbreviated financial statements) details of debts and credits (Payables to Suppliers, Other Payables, Customer Receivables, Payables to Banks, ..) even if contained only in the Explanatory Notes

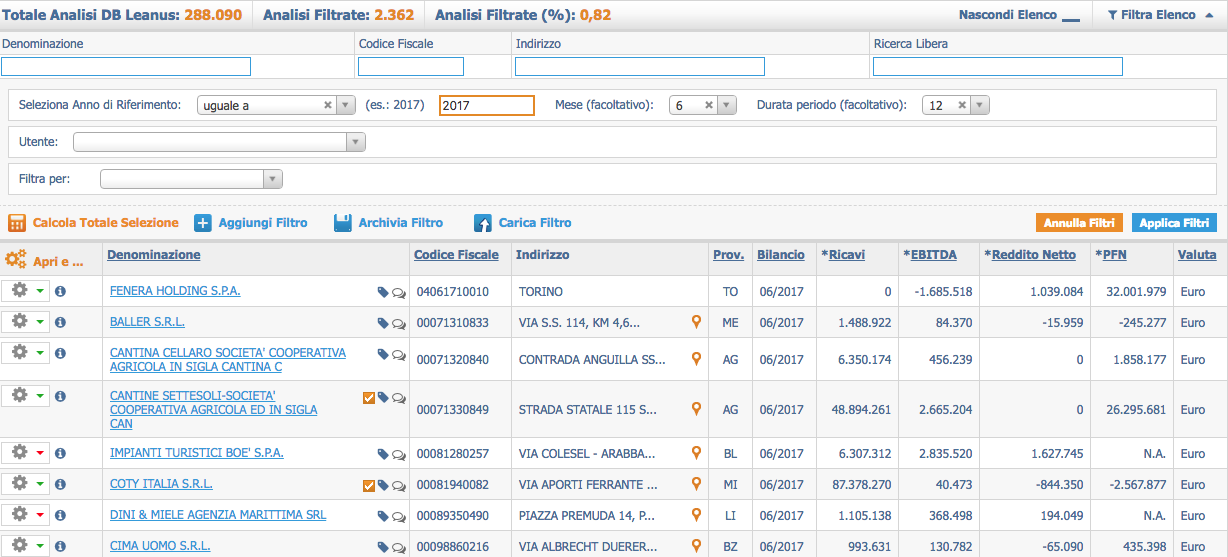

- Indication, for each accounting period, of Month / Year and duration in months, eg. 7/2014 (14) indicates a 14-month financial year ending in July 2014

- Availability of at least two accounting periods consecutive if available in the original financial statements

- Ability to download directly from the Business Register any balance sheet or accounting situation that may not be available in the batch supply

- Availability of the standard civil format or with an identical number of lines for the Income Statement and Balance Sheet for all the financial statements regardless of the value of the individual accounts

- Availability of different formats (Eg. XLS, XML, XBR extension etc.)

- Ability to extend the analysis to 10 years and beyond.

- The availability of the electronic format (XML, XBR extension, XML etc.) also of the financial statements in PDF relating to subjects not obliged to file financial statements in electronic format

- Ability to transfer financial statements, parts of them or reclassified both with single downloads, via Web Services and in Batch

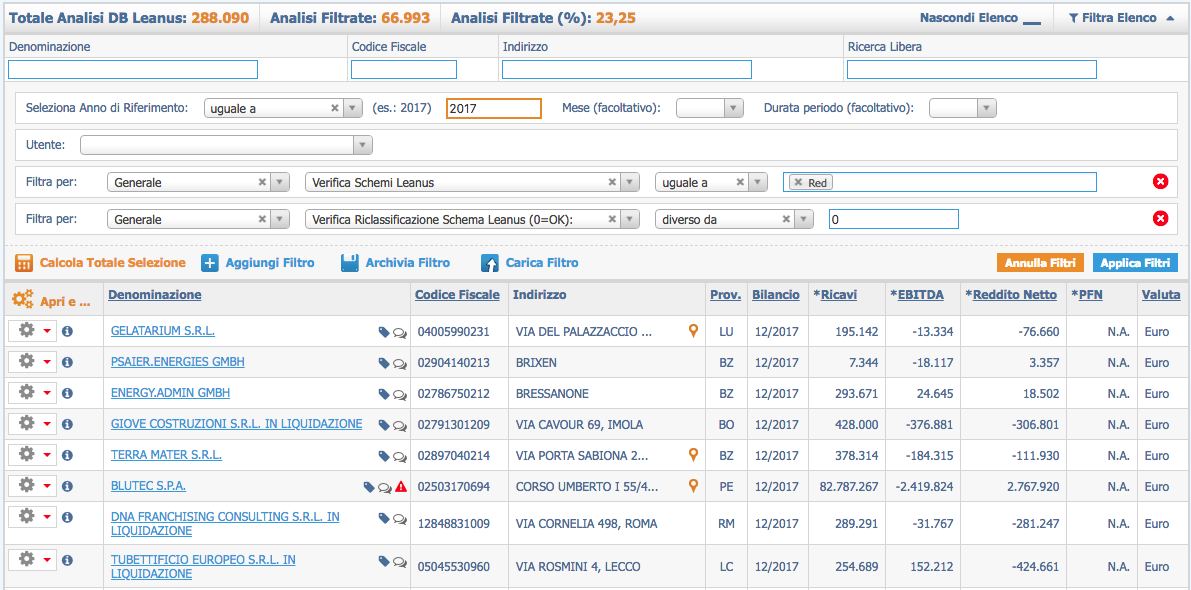

Financial statements which for at least one accounting period do not present all the details of payables and receivables

Financial statements that in 2017 do not present all the details of payables and receivables

Subjects with both ordinary and consolidated financial statements

Examples of financial statements that close the financial year in a period other than 31.12.20XX and have a duration other than 12 months

If you want help assessing the quality of your supply, contact us.

Post your feedback on this topic.